Income Tax Return – Documents, Forms and How to File ITR Online AY 2023-24

In India, it is mandatory for all taxpayers who earn more than the basic tax exemption limit to file their income tax returns or ITR for a financial year with the Income Tax Department. The ITR needs to be filed within the due date, which is typically 31st July of the following financial year. Continue reading to know what is ITR, how and when to file it, the documents required, and more.

What is Income Tax Return (ITR)?

An ITR is a form that you must fill up to declare your gross income for a particular financial year, report your net tax liabilities, and claim refunds if you have paid excess tax for the year. Section 139(1) of Income Tax Act, 1961 states that registered taxpayers below 80, whose income exceeds the basic exemption limit (of ₹2.5 lakh or ₹3 lakh – as per their tax regime), must submit the ITR form on the Income Tax website. Taxpayers, above 80, can file paper-based ITRs.

Why Should You File ITR?

1. Helps Expedite Visa Approval

If you’re planning a foreign trip, the visiting country could ask for your income proof in order to issue a visa. Especially, countries, such as the US, the UK, and some European nations, will mandatorily ask for your income tax return in order to process and approve your application.

2. Helps With Loan Approval

Many lenders and credit card issuers may ask for your ITR returns for the last three years along with other supporting documents in order to approve your application or offer favourable terms of repayment.

3. Claim Tax Refunds

If your employer deducts tax exceeding your actual liability for the year, you can claim it later after filing your income tax return as a refund. The Income Tax Department, after adjusting the total TDS paid against your net tax liability, will refund the excess amount to a bank account that you have linked.

4. Carry Forward Losses to the Next Financial Year

If you incur losses under the heads “Capital Gains” or “Profits or Gains from Business or Profession”, you can carry forward the losses to the next financial year as per the provisions of Section 70 and 71 of the I-T Act. But you need to file your ITR to do so.

5. Could Help With Inheritance In Case a Taxpayer Passes Away

When a taxpayer passes away, the income tax returns filed by them during their lifetime serve as a record of their assets and liabilities. This can help with easy distribution of assets among the legal heirs.

6. Helps Meet Eligibility for Government Tenders

One of the most important eligibility criteria for participating in a government tender process is to have ITR records for the past few years. So, if you want to file a tender for a government project, you must file ITR returns every year.

7. Could Act as Proof of Address and Income

Since self-employed professionals do not get a salary slip, they can use their ITR records as proof of income and address.

8. To Get a Tax Clearance Certificate

Certain high-value transactions, like transfer or sale of an asset in India by a foreigner, require a tax clearance certificate from the Income Tax Department. However, in order to obtain a tax clearance certificate, you will need to first file ITR returns.

Who Should File ITR?

It is compulsory for an Indian citizen to file an Income Tax Return if:

- Their gross income, or their income before any taxes or deduction, exceeds the basic exemption limit of:

- ₹2.5 lakh, for those below 60 years

- ₹3 lakh, for those between 60 and 80 years

- ₹5 lakh, for those above 80

- They have paid excess tax and want to claim a refund for the same

- They have earned an income from foreign assets during a financial year

- They want to apply for a loan or a visa

- They are a business entity

- They want to carry forward a loss

- They are a foreign company operating in India and receiving benefits under a special treaty

- They are a Hindu Undivided Family (HUF), Association of Persons (AOP), or Body of Individuals (BOI) who earn more than the prescribed exemption limit

You may have to file an income tax return even if your earnings don’t exceed the applicable basic exemption limit if:

- You have deposited a lump sum of above ₹1 crore in one or more current accounts in a financial year

- You have spent ₹2 lakh or more on a foreign tour

- You have spent more than ₹1 lakh in electricity bills in a financial year

What are the Documents Required to File ITR?

- Salary slips

- PAN

- Aadhaar

- Passbooks or statements issued by your bank, post office, and/or Public Provident Fund (PPF)

- Interest certificates issued by your bank

- Investment proofs, against which you have claimed deductions

- Home loan statement, if applicable

- Form-16: TDS certificate issued by your employer, detailing the salary paid and the tax deducted

- Form-16A: For tax deducted on income other than salary, such as interests earned from recurring deposits, fixed deposits, etc.

- Form-16B: Issued by the buyer of a property you have sold, showing that TDS was paid on the amount received by you

- Form-16C: Issued by your tenant, if applicable. It proves that TDS was deducted on the rent received by you

- Form-26AS: This is a consolidated annual tax statement, which provides details of the taxes paid against your PAN number

Also Read

How to File ITR for AY 2023-24 Online?

Follow the steps below to file your ITR online for Financial Year 2022-23 or Assessment Year 2023-2024:

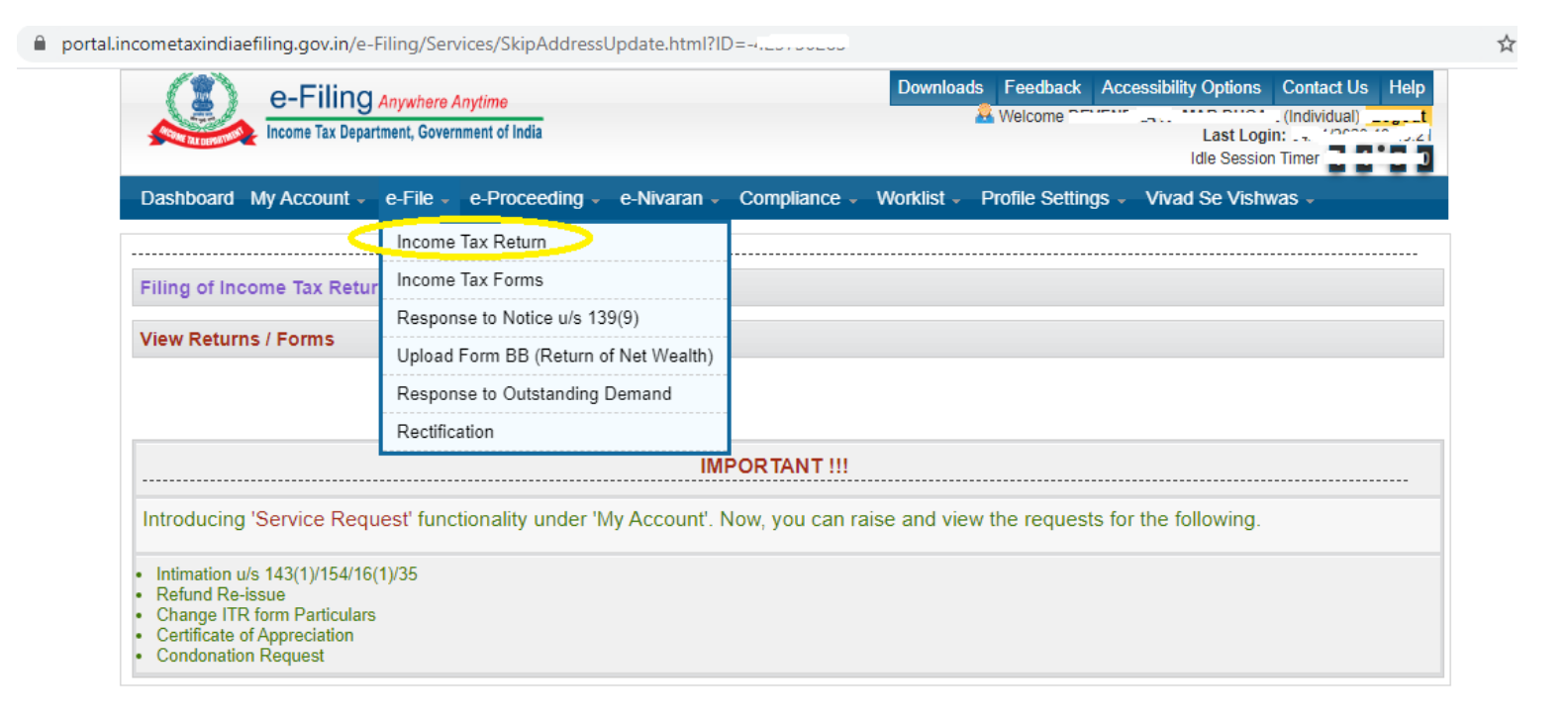

- Visit the Official Income Tax Portal

Log into the Income Tax e-Filing by clicking on the e-File menu and select ‘Income Tax Return’

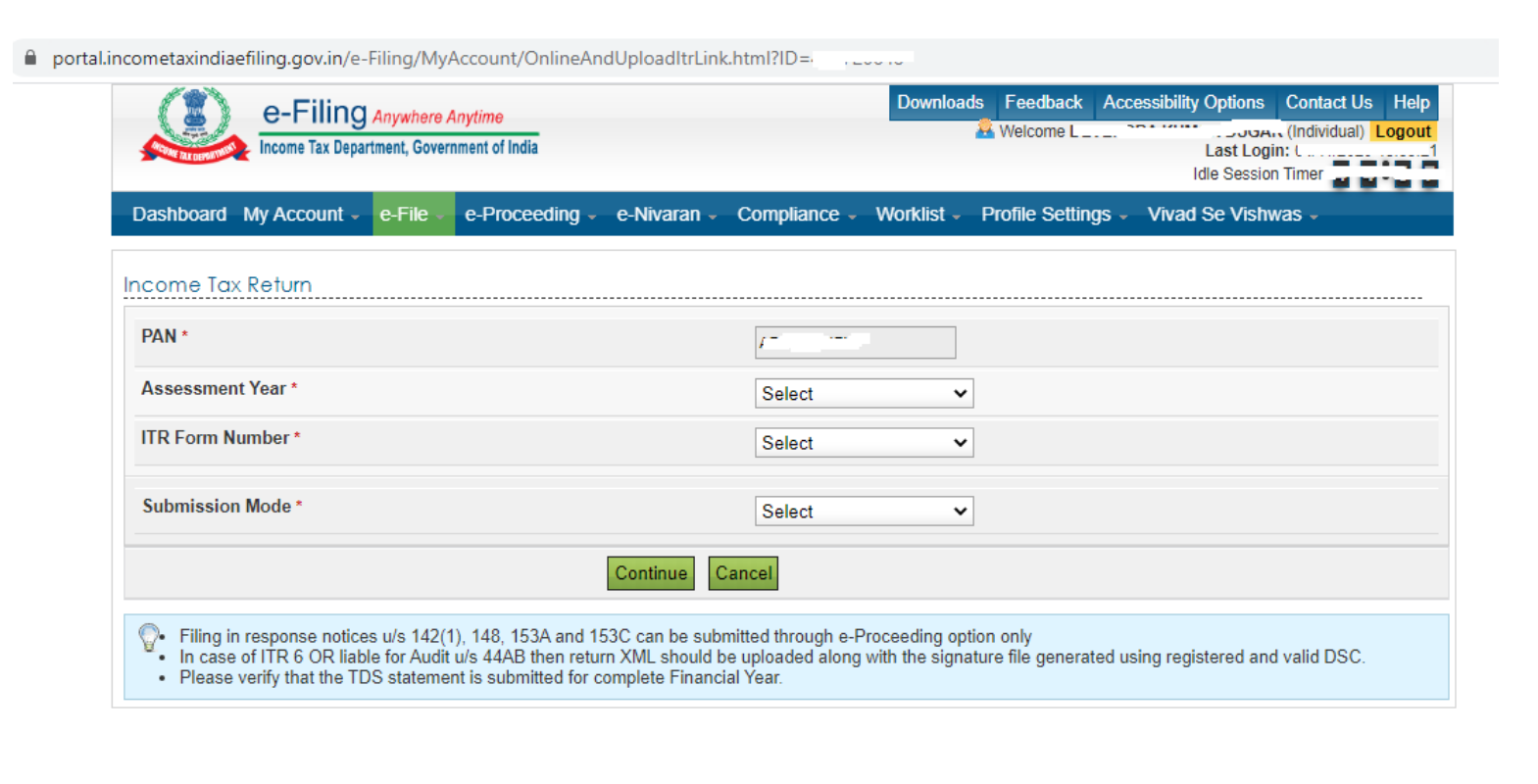

- Select Your Submission Mode

Select the assessment year, form type, filing type, and set the submission mode to ‘online’. Finally, click on ‘Continue’.

- Enter Your Reason for ITR Filing

From the options listed in the drop-down menu, choose the reason for which you are filing ITR.

- Enter Your Bank Details

You could either validate your existing banking information or link a new bank account.

- Verify or Update Your Personal Information

You will be redirected to a new page. Most of the details on this page will be pre-filled. Verify/update the information and add information in the blank fields.

- Choose Your Preferred Mode of Verification

‘Submit’ the ITR form and choose your preferred mode of verification. You could either choose to verify the submission with an electronic verification code (EVC) or with an Aadhaar OTP. Or you could send a self-attested physical copy of your ITR form to CPC Bangalore.

Which Form to Use for Filing ITR?

The type of ITR form you need to submit will depend on the type of income you earn. You could easily choose and fill the right ITR form from the official Income Tax website. The different types of ITR forms available are as follows:

1. ITR-1 or Sahaj

This form is to be filled up by an individual who has an annual income of up to ₹50 lakh. The income could be from a salary, from one house property, agricultural income of up to ₹5,000, from a family pension scheme, among other sources, including:

- Interest from income tax refund

- Interest from a savings or deposit scheme

- Interest received from increased compensation

- Any other interest income

2. ITR-2

Any individual or HUF must fill this form if they are not eligible to file ITR-1 and who do not have any profit from a business or a profession. Those making profits through the following means won’t be eligible to file ITR-2:

- Interest

- Salary

- Bonus of some kind

- Remuneration or commission received from a partnership-based firm

3. ITR-3

This form should be used to file their income tax return by an individual or a HUF, provided the income falls under the head ‘profits or gains of business or profession’ and who is/are not eligible to file their income tax return with ITR-1, ITR-2 or ITR-4.

4. ITR-4 or Sugam

This form should be filled up by individuals, HUFs, or business firms (other than a limited liability partnership firm) having a total professional income of up to ₹50 Lakh or business income up to ₹2 Crore in a year.

5. ITR-5

This form can be used to file income tax returns by a limited liability partnership firm (LLP), a body of individuals (BOIs), an association of persons (AOPs), a local authority, a cooperative society, a business trust, an artificial juridical person (AJP), an investment firm, or different types of estates as specified under the current tax laws.

6. ITR-6

Any company registered under Companies Act 2013 or Companies Act 1956 must use this form to file their income tax returns, except charitable or religious organisations.

Another notable point is that any company which is liable to file their ITR using this form and whose annual gross revenue exceeded ₹1 Crore in the previous financial year, must also get their accounts audited by a certified chartered accountant.

7. ITR-7

This form must be used by such companies and people who are required to file their income tax returns as per Sections 139(4A), 139(4B), 139(4C), or 139(4D). Generally, entities, such as political parties, religious or charitable trusts, universities and places of higher education, and research institutions are required to fill this form.

Due Date for Filing ITR in AY 2023-2024

For FY 2022-2023 (AY 2023-2024), the due date for filing income tax returns is as follows:

| Taxpayer Type | Due Date * |

| Individual/HUF/AOP/BOI (not requiring an audit services) | 31st July, 2023 |

| Businesses (that require audit) | 31st October, 2023 |

| Businesses (That require a Transfer Pricing Report) | 30th November, 2023 |

The last date for revised or belated return has been set as 31st December, 2023.

Penalty for Late Filing of Income Tax Return

Based on one’s income tax slab, the penalty for late filing of ITR varies as follows:

| Deadline | Penalty, if annual income is up to ₹5 Lakh | Penalty, if annual income exceeds ₹5 Lakh |

| Before 31st July, 2023 (Original Deadline) | Nil | Nil |

| Before 31st December, 2023 (Last date for belated payment) | ₹1,000 | ₹5,000 |

| From 1st January to 31st March, 2024 (Further extension) | ₹1,000 | ₹10,000 |

In addition, an interest rate of 1% will be charged on the pending amount until the day the tax is paid in full.

Moreover, if a taxpayer, who is due for a refund, fails to pay their tax on time, the refund will be delayed.

How to Check Your ITR Status?

You can easily track your ITR status online from the official website of Income Tax – with or without login. Let’s see how each works:

1. With Login Credentials

If you have your login credentials for the Income Tax portal, you can use it to login and check the status of your ITR. However, remember that you should have done at least one I-T return using the e-Filing portal.

Here are the steps:

Step 1: Login to your e-Filing portal account.

Step 2: Go to ‘e-File’, then ‘Income Tax Returns’, and then ‘View Filed Returns’

Step 3: On the ‘View Filed Returns’ page, you can check all the returns filed by you so far. You can also download the ITR-V acknowledgement receipt, the ITR form filed and uploaded by you in the PDF format, and the intimation order.

2. Without Login Credentials

Even if you don’t have a valid password or an ID, or don’t wish to login, you can still check the status of your I-T return using the same portal. However, you should have a valid mobile number to receive a one-time password, which you will have to use for checking the status of your income tax return.

Here are the steps:

Step 1: Visit the Income Tax e-Filing portal homepage.

Step 2: Select and click on the ‘Income Tax Return’ option.

Step 3: Now, you will get redirected to the ‘Income Tax Return (ITR) Status’ page where you have to enter the acknowledgement number you received at the time of submitting your form and a valid mobile number.

Step 4: You will receive an OTP. Enter it in the highlighted field within 15 minutes of receiving it, and click ‘Submit’.

On successful verification of the code, you will be able to see the status of your ITR submission.

Also Read

How to Download the ITR Verification Form?

The ITR Verification or ITR-V form is generated to validate the e-filing. It is applicable only for those who submit their ITR forms without a digital signature. To download your ITR-V form:

Step 1: Visit the Income Tax e-filing website

Step 2: Select the ‘View Filed Returns’ option from the Income Tax Returns drop-down

Step 3: On the next page, you will have the option to download the ITR-V form for the relevant assessment year. Select the year and click on ‘Download Form’

Step 4: If you have not e-verified your ITR submission, you can download the ITR-V form and send a self-attested copy of the same to CPC Bangalore within 120 days of submitting your form

Benefits of E-filing Income Tax Return

- It is an auto-fill process, which means quick, convenient and error-free processing

- You will receive an immediate confirmation upon successful submission of ITR

- You can do it anywhere, anytime

- You can easily track the status of your ITR through the Income Tax portal.

- E-filing is considerably more secure as compared to paper filing

- Using netbanking, you can ensure seamless transfer of funds – both refunds, if any, and payment of outstanding taxes, if applicable

Final Word

Now that you know the ITR meaning, how to file an ITR, the penalties of not filing on time, we are quite sure that you will watch out for ITR filing deadlines and ensure that you are contributing to the growth and progress of the country by paying your taxes in time.

That said, did you know that by investing in Navi ELSS Tax Saver Nifty 50 Index Fund, you can not only save taxes of up to ₹46,800 per year under Section 80C but also increase your returns potential, with exposure to India’s 50 largest companies? To get started, download the Navi App today.

FAQs

Sections 44ADA, 44AE, and 44AD offer a presumptive income scheme wherein a company or an individual can compute their earnings on a notional basis. This means that the earnings are presumed at a specific rate (minimum) depending on the proportion of gross turnover/receipts or on the basis of owning commercial vehicles. However, a taxpayer must file ITR-3 if his/her business turnover is above Rs. 2 crores.

No, it is not compulsory to attach documents (such as investment statements or TDS proofs) to your ITR forms. However, taxpayers must keep such documents ready since the Income Tax Department may ask to submit the details during enquiry or assessment.

To simplify the tax payment procedure, the IT department has introduced a website wherein companies and individuals can submit IT returns at their own convenience. You need to visit the e-filing portal of the Income Tax Department to file your tax returns. This website doesn’t charge anything to facilitate e-filing.

You need to keep the following documents handy while filing ITR:

1. Information related to investments

2. Form 16

3. Bank account details

4. Aadhaar card

5. PAN card

6. Salary slips (for employees)

7. TDS certificate

8. Statement of interest in case of fixed deposits

9. Savings account bank statement showing interest income

10. Form 26AS

Section 80C provides a tax deduction of Rs. 1.5 lakh (maximum) for specific investments. The tax benefit is available for investing in LIC, ELSS, PPF, etc. Moreover, taxpayers can claim deduction under this section for incurring certain expenses, for example, paying registration fees and stamp duty when purchasing a house.

Yes, it is mandatory to file ITR, if your annual income exceeds the basic tax exemption limit. However, even if it doesn’t, you should still consider filing a return to enjoy other benefits, such as easier loan approval, faster visa approval, and more.

If you are liable to file an income tax return and don’t, you will have to pay a hefty fine.

Disclaimer

This article is solely for educational purposes. Navi doesn't take any responsibility for the information or claims made in the blog.

Read More on Income Tax Act