Prime Minister’s Employment Generation Programme (PMEGP) – How To Apply Online

In August 2008, the Indian government approved the implementation of a new credit-linked subsidy program known as the PMEGP (full form – Prime Minister’s Employment Generation Programme). The PMEGP scheme was brought to life by combining two existing schemes – Prime Minister’s Rozgar Yojana (PMRY) and Rural Employment Generation Programme (REGP) and was launched by the Ministry of Micro, Small, and Medium Enterprises. This was done primarily to generate employment opportunities in the non-farm sector for rural and urban areas.

Under this scheme, a beneficiary invests 5-10% of the total investment and the government provides a 15-35% subsidy based on the applicant’s eligibility. State KVIC (Khadi and Village Industries Commission) Directorates, District Industries Centers (DICs), State Khadi and Village Industries Boards (KVIBs) and banks are responsible for implementing the PMEGP scheme at the state level. The KVIC can route government subsidies through designated banks for subsequent disbursement directly into the beneficiaries’ or entrepreneurs’ bank accounts. Read on to know the PMEGP loan interest rates, eligibility, documents, banks’ list and how to apply.

Objectives of the PMEGP Scheme

PMEGP has proven beneficial in boosting the growth of the MSME sector and, as a result, improving the country’s economic situation. It was implemented to meet the following objectives:

- To create employment opportunities in rural and urban areas by establishing self-employment ventures.

- To provide long-term sustainable self-employment opportunities for the dispersed traditional and potential craftsmen, artisans, and unemployed youth to reduce rural migration to urban areas.

- To increase the income capacity of workers and artisans and increase the rate of rural and urban employment growth.

Subsidy Under PMEGP Scheme

Beneficiaries may be eligible for a government subsidy ranging from 15% to 35% of the project cost. The funds available under the PMEGP Scheme are based on levels of support in urban and rural areas according to the category:

1. For setting up a new micro-enterprise unit

| Beneficiary Category | The Share of Beneficiary(Of Total Project) | Rate of Subsidy(From Govt.) – Urban | Subsidy Rate (From Govt.) – Rural |

| General | 10% | 15% | 25% |

| Special | 5% | 25% | 35% |

The maximum cost of a project admissible for margin subsidy in the manufacturing sector is up to Rs.25 lakh, and in the business or service sector is Rs.10 lakh. The bank provides the balance of the total project cost under this scheme as a term loan.

2. For 2nd loan for upgradation for existing PMEGP/REGP and MUDRA units

| Categories of beneficiary under PMEGP( for upgradation of existing unit) | Beneficiary’s contribution (for project costs) | Rate of subsidy (for project costs) |

| All categories | 10% | 15% (20% in NER and hill state) |

- The maximum cost of a project admissible for margin subsidy in the manufacturing sector for up-gradation is up to Rs.1 crore.

- The maximum PMEGP subsidy offered under the manufacturing sector is Rs.15 lakh and Rs.20 lakh in the north-eastern states/hill states.

- The maximum cost of a project admissible for margin subsidy in the business or service sector for up-gradation is Rs.25 lakh.

- The maximum PMEGP subsidy offered under the business or service sector is Rs.3.75 lakh and Rs.5 lakh for NER/hill stations.

The bank provides the balance of the total project cost under this scheme as a term loan.

PMEGP Loan Interest Rate

Under the PMEGP scheme, a standard interest rate is charged, but the rate of interest and subsidy offered varies across banks. It is calculated based on the applicant’s profile, their creditworthiness, repayment capacity, financial stability, business tenure, cost invested, and total project cost. PMEGP loan interest rates usually range between 11 and 12%. With an initial moratorium prescribed by the bank or financial institution, the repayment schedule typically ranges between 3 and 7 years.

Eligibility Criteria for PMEGP Loan

- Individuals over 18 years of age are eligible to participate in the scheme.

- Applicants must have passed at least the 8th standard to set up projects over Rs.10 lakh in the manufacturing sector and more than Rs.5 lakh in the business or service sector.

- There is no income limit for PMEGP scheme project establishment assistance.

- Only one person from each family is eligible to receive financial assistance for project development under the PMEGP.

- Only new projects sanctioned specifically under the PMEGP are eligible for assistance under the scheme.

- Self-Help Groups, including those from BPL households, are eligible if they have not received benefits from any other scheme.

- Institutions incorporated under the Societies Registration Act of 1860. Cooperative societies and charitable trusts are also eligible.

- Existing or newly established units under PMRY, REGP, or any other federal or state government scheme are ineligible.

- Enterprises previously receiving government subsidies under any other central or state scheme are ineligible.

- Projects with no capital investment are ineligible for financing under the scheme. Projects worth more than Rs.5 lakh that do not require working capital need approval from the Regional Office or Controller of the Bank’s Branch.

Documents Required for PMEGP Loan

The following list contains the documents required for PMEGP loans for a smooth process:

- In the case of special categories, a certified copy of the caste or a community certificate or any other relevant document is issued by a competent authority.

- All borrower KYC documents for information input into the PMEGP e-portal, including Aadhaar, PAN, EPIC, etc.

- Wherever possible, a certified copy of the institutions’ by-laws must be attached to the margin money (subsidy) claim.

- Projects over Rs.5 lakh that do not require working capital need approval from the Regional Office or Controller of the Bank’s Branch. Subsidy claims must be submitted with a certified copy of such approval from the Regional Office or Controller.

How To Apply for a PMEGP Loan Online?

Prospective beneficiaries are invited to submit applications, along with project proposals, for establishing an enterprise or launching service units under the PMEGP. Local advertisements in print and electronic media inviting applications in consultation with KVIB and the respective state’s Director of Industries (for DICs) are issued by the State/Divisional Directors of KVIC.

Beneficiaries can also apply for a PMEGP loan online at their official website.

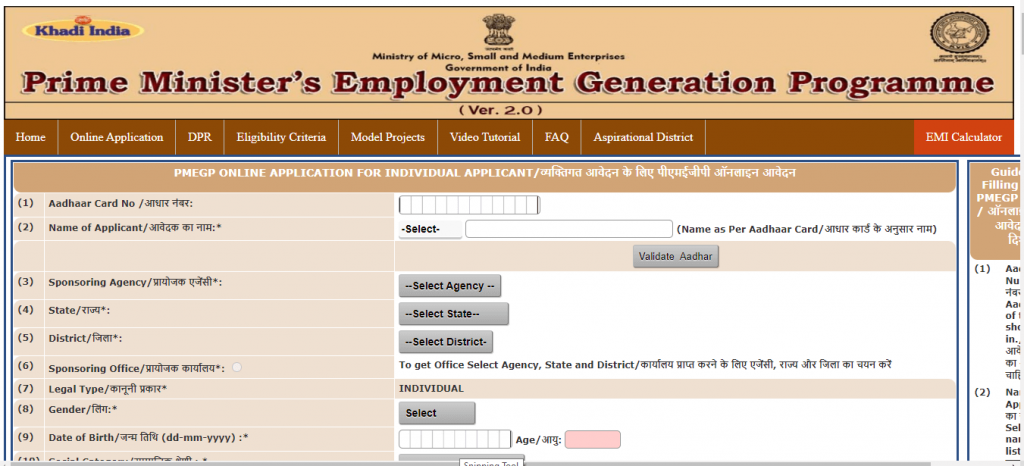

Step 1: Follow the instructions for completing the online PMEGP application and enter all the required information.

Step 2: After entering all the required information, click ‘Save Applicant Data’ to save the completed details.

Step 3: After saving your data, you can upload all of the documents for the application form’s final submission.

Step 4: An application ID number and password are sent to the registered email address for future use.

You can also apply for a PMEGP loan in offline mode. You can print out an application from their official website and submit the filled application to the respective office along with the Detailed Project Report and other required documents.

Also Read: Pradhan Mantri Jan Arogya Yojana: PMJAY Scheme Features And Eligibility Criteria

PMEGP Bank List 2022

Financial institutions under the PMEGP scheme are:

- Banks in the public sector

- Banks in the public sector

- The State Level Task Force Committee that is headed by the Principal Secretary (Industries) or the Commissioner approves cooperative banks (Industries)

- Private Sector Scheduled Commercial Banks that are approved only by the State Level Task Force Committee and led by the Principal Secretary (Industries)/Commissioner (Industries)

- SIDB (Small Industries Development Bank of India)

Some of the banks under the PMEGP loan are listed below:

| IDFC First Bank | Bank of Baroda |

| Indian Bank | Bank of India |

| Kotak Mahindra Bank | Canara Bank |

| Punjab National Bank | Central Bank of India |

| State Bank of India | HDFC Bank Ltd. |

| UCO Bank | ICICI Bank Ltd. |

| Union Bank of India | Axis Bank |

Also Read: PMAY Credit Linked Subsidy Scheme (CLSS) Benefits & Calculation Of Interest Subsidy

Final Word

Central Government schemes such as the Prime Minister’s Employment Generation Programme (PMEGP) have opened new avenues for developing and promoting employment and entrepreneurship in the micro sector. The PMEGP scheme assists traditional artisans and unemployed youth in rural and urban regions in establishing non-farm micro-enterprises. The bank evaluates the project, decides based on its viability, and grants a loan.

The scheme has proven to be advantageous at a time when the economy is still recovering from the effects of the COVID-19 pandemic. The PMEGP loan provides many individuals and businesses in the country with a much-needed credit infusion.

FAQs

Ans: Up to Rs.25 lakh in the manufacturing sector and Rs.10 lakh in the service sector for setting up a new micro-enterprise.

Ans: No. Banks provide the balance of the cost of the project in the form of credit facilities and working capital.

Ans: Loan, working capital, and 10% of the project cost as an own contribution in the case of the general category, and 5% of the project cost in the case of the weaker section.

Ans: According to RBI guidelines, projects worth up to Rs. 10 lakhs are exempt from collateral security under PMEGP loans.

Ans: The lock-in period of government subsidies is 3 years.

Personal Loan in Your City