What is Bill of Exchange: Definition, Types, Examples and Format

What is a Bill of Exchange?

A Bill of Exchange is a written order to pay a specified amount of money to the maker or bearer of the bill. A bill of exchange, under the Negotiable Instruments Act, 1881, is payable either at a specified date or on demand as mutually agreed upon by the involved parties. Read on to know how it works, what are its features, pros, cons and differences with a promissory note.

Parties to a Bill of Exchange

Primarily, there are three parties in a Bill of Exchange. They are as follows:

1. Drawer

The person or business who draws the Bill and to whom the money is owed

2. Drawee

The person or business on which the Bill is drawn or who is owing money to another

3. Payee

The person who would receive the payment for the Bill

Usually, the drawer and the payee are the same persons or entities if the Bill is retained till the specified date. However, the drawer might transfer the Bill to another party, in which case, the other party would become the payee.

How Does a Bill of Exchange Work?

If an individual or an entity is owed money for goods or services sold or delivered, they might draw a Bill of Exchange to secure the payment. The individual or entity would be called the maker or drawer of the Bill and the person or business that owes the money would be called the drawee.

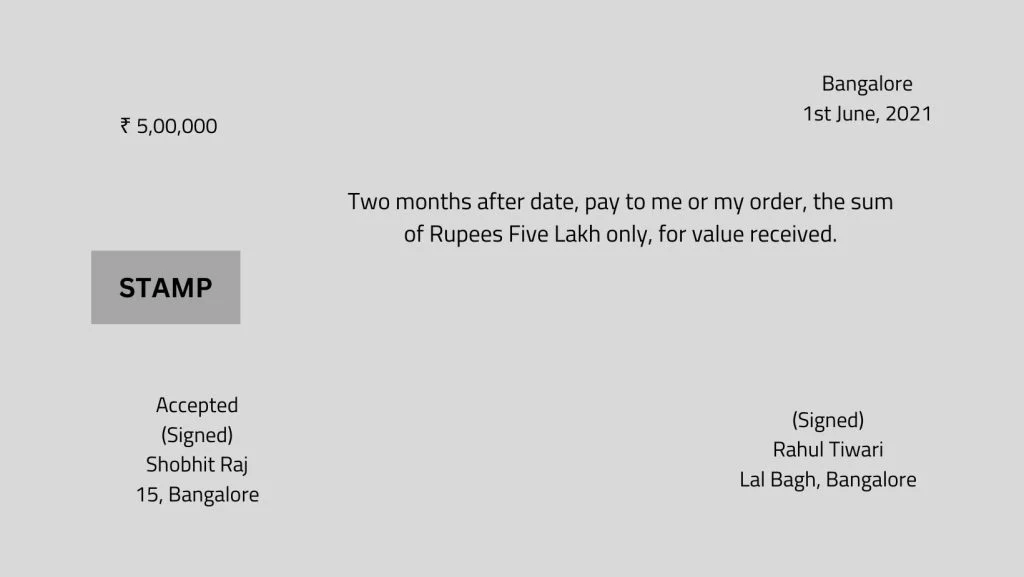

The drawer would draw the bill of exchange stating the following:

- Name of the drawee

- The unconditional order of payment

- The payment date (if the bill is payable on a specific date). If not, the date would not be mentioned. The bill of exchange would be payable on demand

- The amount of payment

The drawer would then sign the bill of exchange and send it to the drawee making it legally enforceable. After that, the drawer can demand payment from the drawee either on demand or on the specified date by presenting the bill. The drawee would, then, have to honour the bill when presented.

However, if the drawer needs funds before the bill of exchange is to be cleared, he can transfer the bill, at a discount, to a lender. The drawer would get funding against the bill, while the lender can later encash the bill of exchange at the full amount to make a gain.

Bill of Exchange Example

Example 1

- Suppose B owes ₹10,000 to A

- In this case, A would draw a bill of exchange for B for the payment of ₹10,000

- A can draw the bill of exchange stating that he would require the payment after 30 days. If so, B would have to clear the bill and make the payment after 30 days

Example 2

- Suppose A owes ₹10,000 to C

- In this case, A can endorse the bill of exchange in favour of C

- B would make the payment of ₹10,000 to C

Example 3

- Suppose a lender offers ₹9,500 to A against the bill of exchange of ₹10,000 payable after 30 days

- A takes ₹9,500 on the 10th day to meet his financial requirements after submitting the bill of exchange to the lender

- B pays ₹10,000 to the lender after 30 days, and the lender makes a profit of ₹500

Bill of Exchange Format

Important Elements of Bill of Exchange

1. Drawer

An individual or company who makes the bill of exchange

2. Drawee

An individual or company directed to pay the sum of money mentioned in the bill of exchange

3. Payee

An individual or a company who will receive the money

4. Holder

An individual or company who temporarily holds the bill of exchange before providing it to the drawee

5. Acceptor

The drawee, on signing the bill of exchange, becomes the acceptor

6. Endorser

If a party endorses a bill of exchange to another person, that party becomes an endorser

7. Endorsee

The individual to whom a bill of exchange has been endorsed to becomes an endorsed

Also Read

Types of Bill of Exchange

The types of the Bill of Exchange are as follows:

1. Documentary Bill

This bill of exchange comes with documents that authenticate that the transaction took place for which money is owed.

2. Demand Bill

Bills that do not have a specified payment date and are payable on demand are called demand bills.

3. Inland Bill

Bills drawn and honoured in one country are called inland bills.

4. Foreign Bill

Bills that can be paid outside the country are called foreign bills. These bills of exchange are usually used for international trade.

5. Usance Bill

Bills containing a specific time and date of payment are called usance bills.

6. Supply Bill

A bill of exchange that a supplier or contractor withdraws from the government is called a supply bill.

7. Trade Bill

Bills of exchange used in the trade business are called trade bills.

8. Accommodation Bill

A bill of exchange that is drawn and accepted without any condition is called an accommodation bill.

9. Clean Bill

These bills of exchange are not supported by documentary evidence. As such, they carry a higher rate of interest compared to other bills.

Important Features of a Bill of Exchange

Some of the important features of a Bill of Exchange are as follows –

- The bill of exchange is a legal document

- It must always be in writing with proper stamp

- The parties to the bill must be named therein

- The amount of payment is clearly stated in a bill of exchange

- It is not a payment request but an order

- A bill of exchange must be signed by the drawer as well as the drawee

- A bill of exchange must clearly state the date at which the payment needs to be made

- The amount mentioned in a bill of exchange must be paid on-demand or at the end of the stated fixed time

- A bill of exchange payment must be paid in legal tender currency of the specific country

- The drawer and the drawee cannot be the same person

Advantages of a Bill of Exchange

Drawing up a Bill of Exchange has its own set of advantages. These advantages are as follows –

1. Secures Payment

The Bill of Exchange ensures that the creditor would pay the debtor. It serves as a safety net for businesses or individuals to whom money is owed. Moreover, when a specific date is mentioned, debtors can expect payment by that date and manage their cash flow requirements.

2. Can be Discounted for Instant Funding

The Bill of Exchange offers a discounting facility wherein debtors can encash the Bill with a third party, at a discount. They get immediate funds without waiting for the bill’s specified date. On the other hand, the third party offers a reduced amount and can get the Bill cleared at the original amount, thereby making a gain in the process.

3. Can be Endorsed

You can endorse the Bill in that individual’s name if you owe another individual. Such endorsements allow businesses to lower their existing debts.

4. Easy to Issue

The Bill of Exchange can be easily drawn and remitted to the creditor for acceptance. There is a simple Bill of Exchange format that drawers can use to draw the bill.

5. Holds Legal Identity

The Bill is a legal document that mandates the drawee to pay the specified amount on demand or at a specified date. In the case of a default, the drawer can take legal action against the drawee.

Also Read

Disadvantages of a Bill of Exchange

Though beneficial, a Bill of Exchange also has its own set of drawbacks such as:

- Though discounting allows quick funds, the discount paid for the Bill of exchange is an added expense for the drawer

- It can be a short-term mode of securing payments from creditors

- The drawee becomes legally bound to clear the payment on demand or on the specified date

- The discount on a bill of exchange is an additional cost to parties

- It’s an additional burden for the drawer if a bill of exchange is not accepted

Transferability of Bill of Exchange

A bill of exchange could be transferable, so the drawee might have to pay an entirely different party than he/she/it initially agreed to pay. The payee too can transfer a bill of exchange to another endorsee.

Bill of Exchange Risks

There could be a risk that the drawee may not pay as per the bill of exchange. If the drawee refuses to pay on the due date, the bill of exchange could be dishonoured. That’s why it’s extremely important to verify the credibility of all the involved parties in advance.

What is a Promissory Note?

A promissory note is a signed legal document with a written promise to pay the stated amount of money to a specified party or the bearer on the specified date or on demand. It is, however, a negotiable instrument.

Difference between a Promissory Note and a Bill of exchange

| Promissory Note | Bill of Exchange |

| In essence, they are a promise of payment | In essence, they are an order of payment |

| They involve two parties – the drawer and the payee | They could involve three parties – drawer, drawee, and payee (however, drawer and payee could be the same) |

| They need not be accepted by the drawee to be legally binding | They must be accepted by the drawer to be legally binding |

| Primary liability with drawer | Secondary liability with drawer |

| No notice on dishonour | Notice to every party on dishonour |

| The drawer and payee cannot be same | Drawee and payee can be same |

Final Word

As a business or an individual, if a creditor owes you money, you can secure your debt with the help of a bill of exchange. Draw a bill of exchange stating the debt and the debtor’s details and get the debtor to accept it. Once accepted, the bill becomes a legal document and secures your debt payment. If you need funds before a bill of exchange is due, you can discount the bill with a financial institution and get access to funds for your business.

And if you’re looking for urgent cash for your business, you might want to consider an instant Navi Cash Loan of up to ₹20 lakh starting from 9.9% p.a. Just download the Navi app, enter basic details like PAN and Aadhaar, check loan eligibility, complete KYC verification and get the loan amount in your bank account in a few minutes!

FAQs

No, usually, no interest is charged on the Bills of Exchange. However, in certain cases, the Bill might carry an interest.

The Bill of Exchange is quite different from a Promissory Note. The differences are as follows:

-The Bill is drawn by the debtor while the Note is drawn by the creditor

The Bill states an order for the drawee to pay. The Note contains an undertaking by the drawer to pay

The drawee should accept the Bill of Exchange. This acceptance is not required for the Promissory Note:

The drawer and payee of the Bill can be the same. The drawer and payee of the Note can never be the same

The Bill can have multiple copies while the Note cannot.

If the drawee is unable to pay the amount stated on the Bill on demand or on the specified date, it would be called a dishonour of the Bill. On such a dishonour, a notice is served to all parties to Bill

In case the due date is a National holiday, the Bill would become payable one day before the due date. For instance, say the due date on the Bill is 15th August. In this case, the drawee would have to pay the Bill on 14th August.

The payee is the party to which a bill of exchange is payable.

A bill of exchange could involve three parties – drawer, drawee and payee. However, the drawer and the payee could be same under special circumstances.

The drawer draws or issues thre bill of exchange.

The drawer makes or issues the bill of exchange

A Bill of Exchange is a legally binding written order to pay a specified amount of money at the specified date or on demand to the maker or bearer of the bill.