What is a Solvency Certificate? – Format, Documents Required & How to Apply Online?

What is a Solvency Certificate?

A solvency certificate is a legal document furnishing the details regarding the financial stability and solvency of an organisation or individual. This certification is usually required while dealing with government and commercial offices as they need to verify the financial stature of that respective entity. Banks or revenue departments issue it as per the RBI guidelines for a nominal fee.

Why is a Solvency Certificate Required?

A solvency certificate can be required for multiple reasons. Here are some of the significant purposes of a solvency certificate:

- For government and legal purposes

- Solvency certificate for tenders

- For Visa applications and interviews

- Getting Government and private contracts

In some states, one might also require it for getting admission to medical and engineering colleges.

Solvency Certificate Format

A solvency certificate format is the same for most banks and other issuers. But it may differ a little bit in its style and information from one issuer to another. This also depends on the entity it is being issued for.

Here is a solvency certificate sample to provide more clarity on what a solvency certificate looks like.

This sample is for a business entity issued by a bank. This certificate must be issued on a bank’s letterhead and sealed & signed by a concerned officer in the bank.

What are the Documents Required by a Bank to Issue a Solvency Certificate?

Obtaining a solvency certificate requires a long list of documents. However, please note that this requirement may vary from one issuer to another as well as applicants.

This is a list of the documents usually required to get a solvency certificate:

- Request form

- Copy of passport (if any)

- Savings account statement (if any)

- Current account statement (if any)

- Share investment (if any)

- Mutual fund investment (if any)

- Property valuation certificate from a Chartered Engineer (if any)

- Insurance (if any)

- Provident fund account statement (if any)

- Original Encumbrance Certificate of the property

- Gold valuation certificate, issued by Banker based on weight and value of gold

- Liability amount certificate

- Mortgage certificate

- Land revenue or property tax receipt, whichever is applicable

- Chitta or Patta

- Lease agreement

- Building value

- Net worth certificate issued by Chartered Accountant

- Self-declaration of the applicant

- Passport-size photographs

How to Get a Solvency Certificate?

Application procedures for solvency certificates for most states are the same. The only difference might be the interface of the portal, which is different for every state.

1. Steps to Apply Online:

- Go to Nadakacheri home page and Cick on “Online Application”.

- Under ‘Online Application’, click on ‘Apply Online’.

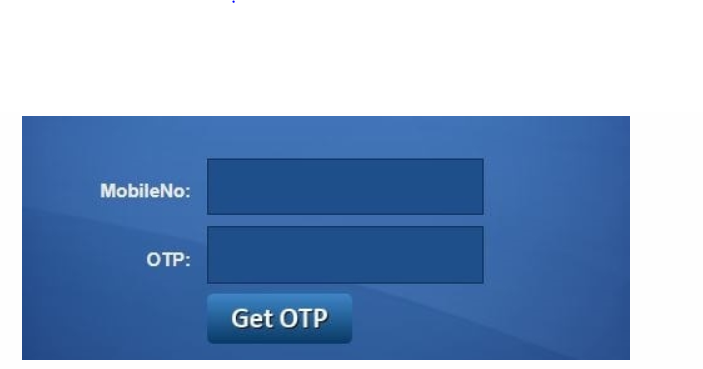

- Enter your mobile number and click on ‘Get OTP’.

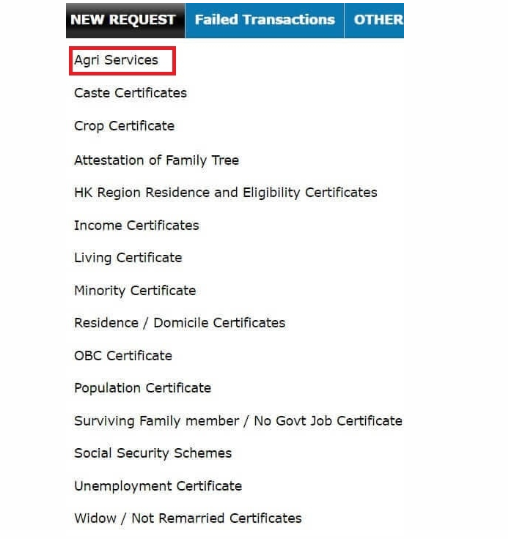

- Under ‘New Request, ‘ click on ‘Services’.

- Choose your language for the certificate and click on ‘Solvency Certificate’.

- Provide your details.

- Select your preferred mode of delivery.

- Upload the documents required and click on ‘Save’.

- Click on ‘Online Payment’.

- Select your Card Type and make the payment

- After successful payment, your acknowledgement number will pop up on the screen. Make sure to note it down for future reference.

2. Steps to Apply Offline:

Step 1: Collect and fill out the solvency certificate application form.

Step 2: Submit the application along with necessary documents at the nearest Revenue or Municipal office.

How to Apply through CSC or e-District Kiosks?

Another way you can apply for a solvency certificate is by visiting a Common Service Centre (CSC) or e-District Kiosk. The steps have been discussed below:

Step 1: Collect the solvency certificate application form and fill it out correctly.

Step 2: Gather the required documents and submit them along with the duly filled form at the nearest e-District Kiosk or CSC.

Who will Issue the Solvency Certificate?

Banks, financial institutions and the revenue department of states have the authority to issue a solvency certificate.

Banks issue this certificate only to their customers based on a few parameters, such as transaction details, account information, and property-related documents available to them. A net worth certificate, which can be obtained from a Chartered Accountant in regard to the applicant’s financial status, also helps in getting a solvency certificate.

A solvency certificate has a validity period which is usually one year. Hence, you have to renew it periodically to keep its validity intact.

Also Read

How to Download the Solvency Certificate?

You can download your solvency certificate from the same website you applied on for the same. You can follow the steps mentioned below:

Step 1: Visit the state website link and click on ‘Check Status’.

Step 2: Enter the application number.

Step 3: Click on ‘Search’.

Step 4: Click on ‘Download certificate’ to get your solvency certificate.

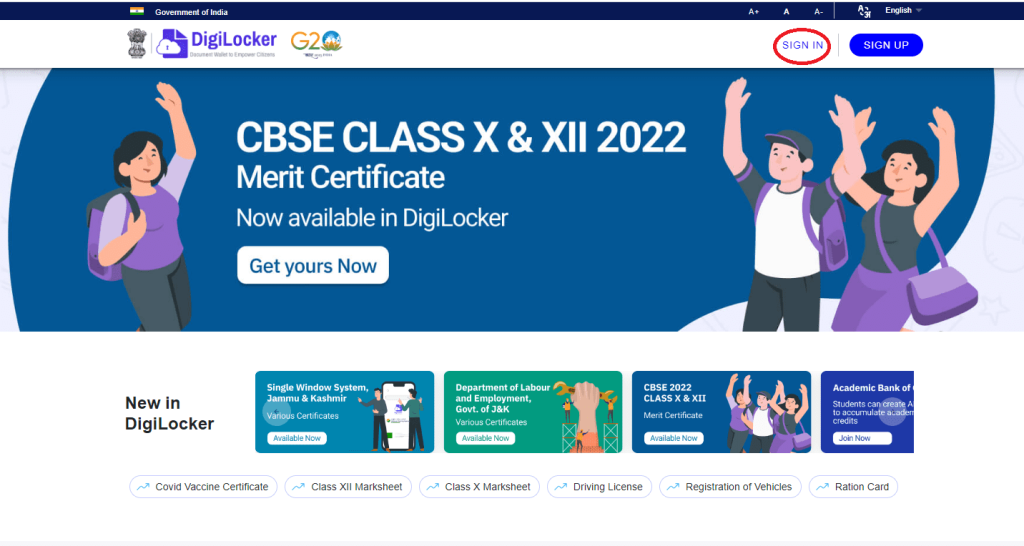

Additionally, another easy way is to get your certificate via DigiLocker. For this, you would need to create a Digilocker account. Once you have one, you need to follow the given steps to download your solvency certificate:

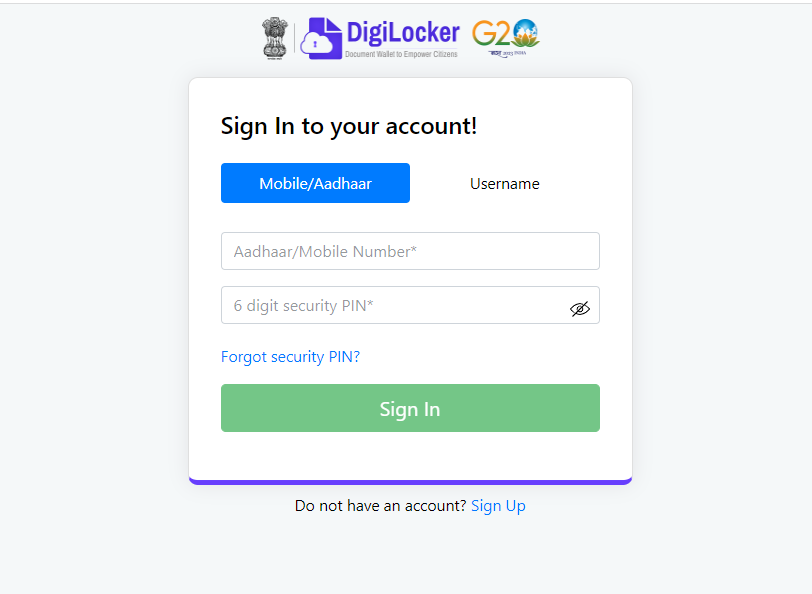

Step 1: Go to the website of Digilocker and Sign in to your account.

Step 2: Sign in with your ID and password, or you can enter your Aadhaar Number to verify through OTP to log in to your account.

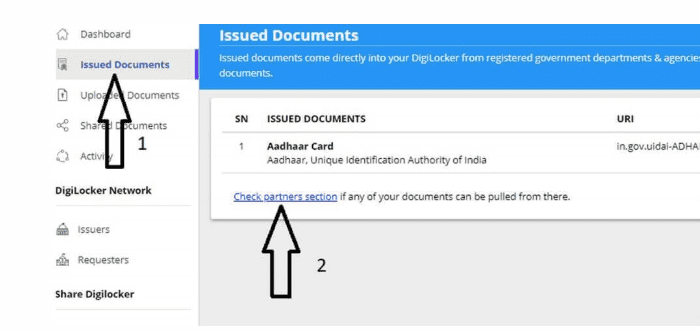

Step 3: Under ‘Issued Documents’, click on ‘Check Partner’s Section.’

Step 4: Select the name of your respective Revenue Department office under ‘Partner’s name’ and service as ‘Solvency Certificate’.

Step 5: Provide ‘Acknowledgement Number’ and click on ‘Accept Checkbox’.

Step 6: Click on ‘Get Document’, and your chosen document will be linked with your DigiLocker Account.

Step 7: Click on ‘Issued Document’ in DigiLocker, and under that, select ‘, View Document’. You will be able to view your solvency certificate.

How to Track the Application Status of a Solvency Certificate?

Tracking the application status of your solvency certificate online involves visiting the same website you applied through. However, the procedure may vary slightly from one state website to another.

Here are the general steps that you can follow to track the solvency certificate application status:

the general steps that you can follow to track the solvency certificate application status:

Step 1: Visit the state government website that provides services related to solvency certificates.

Step 2: Click on ‘Online Application’.

Step 3: Select ‘Application Status’.

Step 4: Enter Application Number and Type.

Step 5: Click on ‘Get Status’, and your application status will be visible in the next step.

Final Word

The solvency certificate has been duly issued and attests to the financial stability and ability of the individual or organisation. With this certificate, the recipient can confidently pursue their financial endeavours and demonstrate their credibility to interested parties.

And if you’re looking for urgent cash at competitive rates, you may consider an instant Navi Cash Loan of up to ₹20 lahks starting from 9.9%. Just download the Navi app, enter basic details like PAN and Aadhaar, check loan eligibility, complete KYC verification and get the loan amount transferred to your bank account in minutes upon approval!

FAQs

In case your certificate is not granted, the Revenue Officer will pass necessary orders regarding the reason for the same. Then, there will be further verification and modification, after which you will receive your solvency certificate.

You can apply to your bank or regional Revenue Officer requesting a solvency certificate. You can also apply to Chief Officer in Charge of Revenue Administration of the concerned & District, Sub-division or Tahasil, Assistant Tahasildar or Assistant District Magistrate.

The fee for a solvency certificate varies from one bank to another. However, most banks charge around Rs. 2000 for a solvency certificate. This fee might also vary from state to state.

Banks and financial establishments are primarily responsible for issuing the solvency certificate. However, the ones that the banks issue are mostly accepted as valid ones. These certificates have a validity period, mostly one year, after which you need to renew them.

After you submit your application with all the required documents, the bank representative who is supposed to verify the documents will complete the process and hand over the certificate. This whole procedure can take about 1 week to get completed. However, this can vary from one state to another.

Solvency certificates are usually valid for 12 months after they are issued.

Most banks in India charge a fee of around Rs.2000 to issue a certificate.