Promissory Note: What it is, Features, Types and Format

Promissory notes are the go-to instrument used by financial institutions to keep a clear and legally enforceable record of loans. A promissory note might not be as detailed as a typical loan agreement; still, it establishes the repayment terms. If you have availed of any credit facilities, you must have signed one as part of the loan application process. Banks also use promissory notes; individuals and businesses essentially use them to obtain funding from sources other than banks.

This article provides a detailed overview of promissory notes, their types, what’s their use and what should a promissory note contain. Read on!

What is a Promissory Note?

A promissory note is a legal document in favour of the lender lawfully binding to the borrower. Through a promissory note, a borrower consents to pay the lender a specified sum of money on a specified date or when demanded. A promissory note consists of all the information related to indebtedness.

The party who makes the promise to pay is called the maker or payer and the party in whose favour the promissory note is made is called the drawer or payee.

A promissory note is a negotiable instrument governed by the Negotiable Instruments Act. A promissory note needs no acceptance, and only two parties are involved.

However, there can be joint borrowers. But promissory notes don’t come with unlimited legal life and are valid only for 3 years, and these 3 years are counted from the date of execution of the promissory note.

How do Promissory Notes Work?

The Geneva Convention of Uniform Laws and Bills of Exchange and Promissory Notes of 1930 monitors the functioning of promissory notes and exchange bills. Promissory notes have the informal tone of an IOU and legal rigidity of a loan contract.

The Geneva Convention of Uniform Laws and Bills of Exchange state the term “Promissory Note” should be mentioned clearly on top of such notes. Like IOU, promissory notes highlight the debt between parties involved. It further adds a promise from the borrower’s end to clear this debt on a specific date.

Like a loan contract, a promissory note legally binds this promise by clearly stating the consequences of defaulting. However, unlike a loan contract’s detailed action of recourse, the latter mentions the penalty charges for missing or late repayments.

When are Promissory Notes Used for?

Promissory notes are used to maintain a legal record of loans. Anyone can use promissory notes; you can even issue promissory notes to your friend from whom you have borrowed short-term credit. That will also count as a valid promissory note.

Generally, promissory notes are used to establish a legal record of mortgages, personal loans, home loans, education loans, auto loans, cash credit limits, etc. Banks and other lending institutions always ask borrowers to create demand promissory notes in their favour to ensure they are paid. A demand promissory note is payable on demand, i.e., when the payee demands the repayment.

Features of Promissory Notes

A promissory note prima facie might appear to be a concise document, but it contains some salient elements that make it outsmart several negotiable instruments.

1. Unconditional Promise

The promise made under a promissory note is not conditional to the happening or non-happening of any event; the promise is unconditional regardless of anything. A conditional promise cannot form the basis for a promissory note.

2. Legal Tender

Promissory notes are always expressed in terms of rupees (in India). A specific amount is present to which no subsequent additions or subtractions could be made.

3. Express Undertaking

Promissory notes are written documents; oral communication of a promise doesn’t constitute a promissory note. Moreover, a promissory note must be expressive enough; a mere acknowledgement of debt is not enough. For example, writing “I owe Rs.10,000 to Mr. X” doesn’t constitute a promissory note. The hand-written note must include some mandatory elements like the legal names of the payee and maker, the amount being loaned / to be repaid, full terms of the agreement and the full amount of liability, etc.

Types of Promissory Notes

The types of promissory notes are given below:

1. Corporate Promissory Note

These promissory notes are for companies that need more cash to pay their creditors. This can happen when their clients still need to pay for their products. By issuing corporate promissory notes, companies assure lenders to pay the due amount on a particular date.

They can also ask for cash from banks with promissory notes and repay them in the future as per the date in the note. Moreover, corporates can borrow money with promissory notes when they exhaust other options. However, such companies pose a high risk of default, which results in high-interest rates. Thus, it can bring high returns to lenders.

2. Investment Promissory Note

Investment promissory notes function like business loans. Both of them help in bringing in funds for the growth of a business. In addition, these promissory notes reduce the chances of defaulting by ensuring borrowers pay their dues on time.

In case borrowers fail to pay their debts, as mentioned in promissory notes, ownership of the company can shift to investors.

3. Real Estate

Real Estate notes are similar to investment notes in terms of defaulting consequences. Ownership of a company moves to investors until all debts are paid.

Under real estate promissory notes, investors can legally take over a company if they cannot repay their loans.

4. Student Promissory Note

Students sign a promissory note when they opt for loans to support their academic careers. According to this note, interest on these loans will not accumulate until graduation or a similar course ends.

Students can sign a master-promissory note to avoid re-signing them every time they take out a loan.

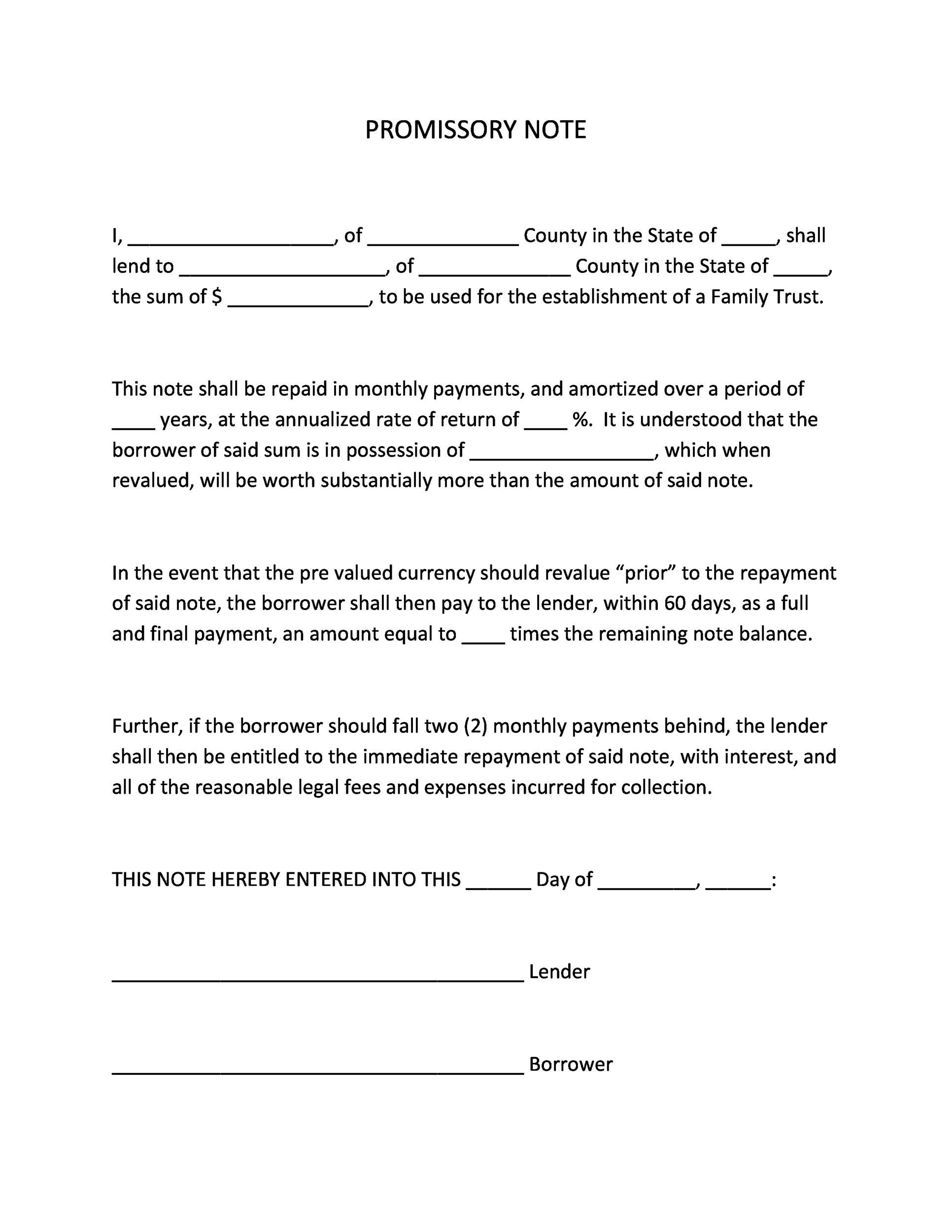

Promissory Note Format

The format of promissory notes varies between institutions. However, given below is a standard template of promissory notes.

Image Source: https://templatelab.com/wp-content/uploads/2016/09/promissory-note-template-38.jpg

Parts of Promissory Notes

A promissory note cannot be legally enforceable unless it contains the following promissory note contents:

1. Name of Parties Involved

The promissory note form should contain the legal name of the payer and the payee as per government records.

2. Amount of Credit

The amount the payer promises to pay the payee.

3. Repayment Date

The date on which the payer will make the repayment. It should be noted that demand promissory notes don’t carry a maturity date as they are payable on demand.

4. Rate of Interest

The rate of interest that the payer promises to pay along with the principal amount. Though promissory notes without the interest element are also valid.

5. Details of Collateral Security Pledged

Secured promissory notes should contain the details of all the goods/services pledged by the payer as a loan guarantee. It could be the description of house property pledged for home loans, a list of gold ornaments pledged for gold loans, etc.

6. Terms of Payment and Default Terms

The payer and the payee must decide the frequency, mode( cash, cheque, RTGS, etc.), and liability of the payer in case of default.

7. Stamped by Revenue

A standard promissory note must be adequately stamped as per the rules of the Indian Stamp Act.

8. Signed

A promissory letter for payment is valid only if all the parties sign it, i.e., the borrower ( co-borrowers if any) and the lender.

Point to Remember Regarding Promissory Notes

- A promissory note is a legally binding instrument issued under Section 4 of the Negotiable Instruments Act, 1881

- Promissory notes must be written by hand with proper mention of all the must-have elements discussed above

- There is no maximum or minimum limit for lending for which loan promissory notes can be issued. You can use it for loans of every quantum

- Promissory notes are valid for 3 years from the date of execution

- Once the payment is made, a promissory note should be crossed or marked as ‘paid in full’

Final Word

Promissory notes are considered a powerful financial instrument due to their simplicity and ability to conform to the requirements of different transactions. Promissory notes put all relevant contract terms in one place and establish a clear and legally binding record between parties. Promissory notes are useful only when you comply with all the underlying conditions; defaulting on terms of promissory notes is not a good idea. Make sure you pay your obligations to avoid your property being confiscated and any legal proceedings.

If you want to avail of a personal loan at flexible EMIs and in a hassle-free process, download the Navi App and apply for a loan up to Rs.20 lakh today!

FAQs

Ans: Promissory notes remain valid for the next three years from the date of execution. Promissory notes are not legally binding on the expiry of such a period.

Ans: Yes, unless expressly stated otherwise, promissory notes are always negotiable instruments. The payee always reserves the right to renounce the promissory note to a third party. The payer will pay to the third party to whom the promissory note is transferred.

Ans: Since promissory notes are legally binding, the payer must pay what he promised to the payee. If he fails to do so, the promissory note will be considered dishonoured. The payee reserves the right to confiscate the security pledged as collateral if it’s a secured promissory note. However, if a dishonoured promissory note is unsecured, the payee can file a lawsuit against the payer.

Ans: For lenders, secured promissory notes are better because their loan is guaranteed by collateral security having a value equal to or more than the loan amount. While for borrowers, unsecured promissory notes are better if given a choice.

Ans: Yes, if it is a demand promissory note. The holder of a demand promissory note can demand the payment from the payer at any time; there is no maturity period. Usually, the payer is served with a notice allowing him a few days to pay the Promissory note.

Personal Loan in Your City

{kind=link}