How to Apply for EPF Loan Online?

Employees’ Provident Fund (EPF) aims to provide a financial cushion for salaried employees after retirement. But did you know that during a financial crisis or any emergency situation, you can partially or fully withdraw the amount from your EPF account to meet your requirements? This is basically termed an EPF loan or loan against EPF.

Read on to know the rules under which you can withdraw the EPF amount, how to apply for it online and offline, the documents required and more.

What is an EPF loan?

An EPF loan is an advance withdrawal of the EPF amount that can be used as a loan to reduce a sudden financial emergency. The Employees’ Provident Fund Organisation has laid down certain conditions under which the EPF amount can be withdrawn in advance. Employees can withdraw from their PF corpus only after EPFO approves their request.

Let’s look at the partial EPF withdrawal rules and regulations first.

How to Apply for EPF Loan Online?

Here are the steps one has to follow to apply for premature withdrawal from EPF online:

- Visit the Official Portal of EPFO

Click on EPFO and log in using UAN and password.

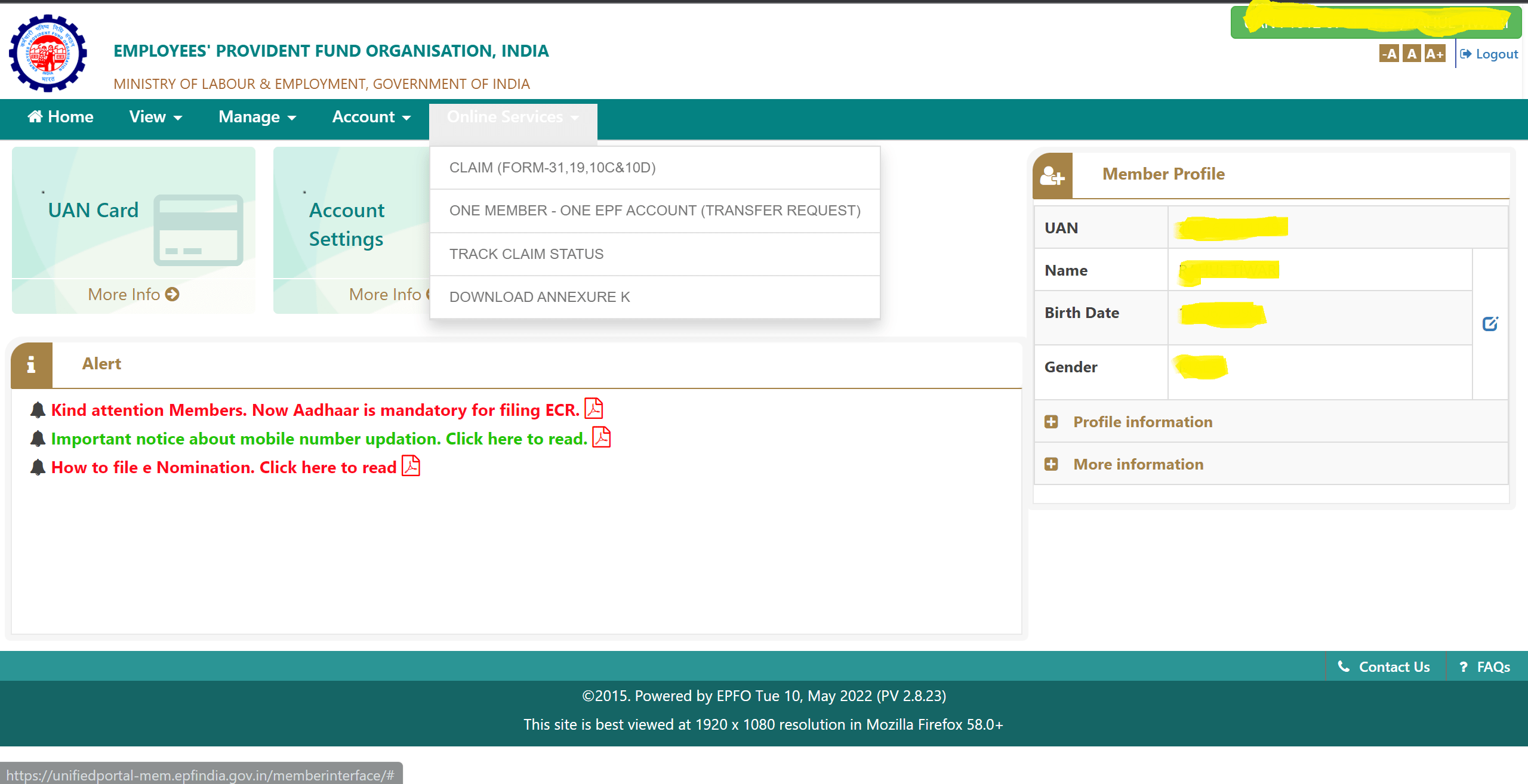

- Click on ‘Online Services’

Scroll down and click on the ‘Online Services’ section. Enter UAN, Name, Birth Date and Gender.

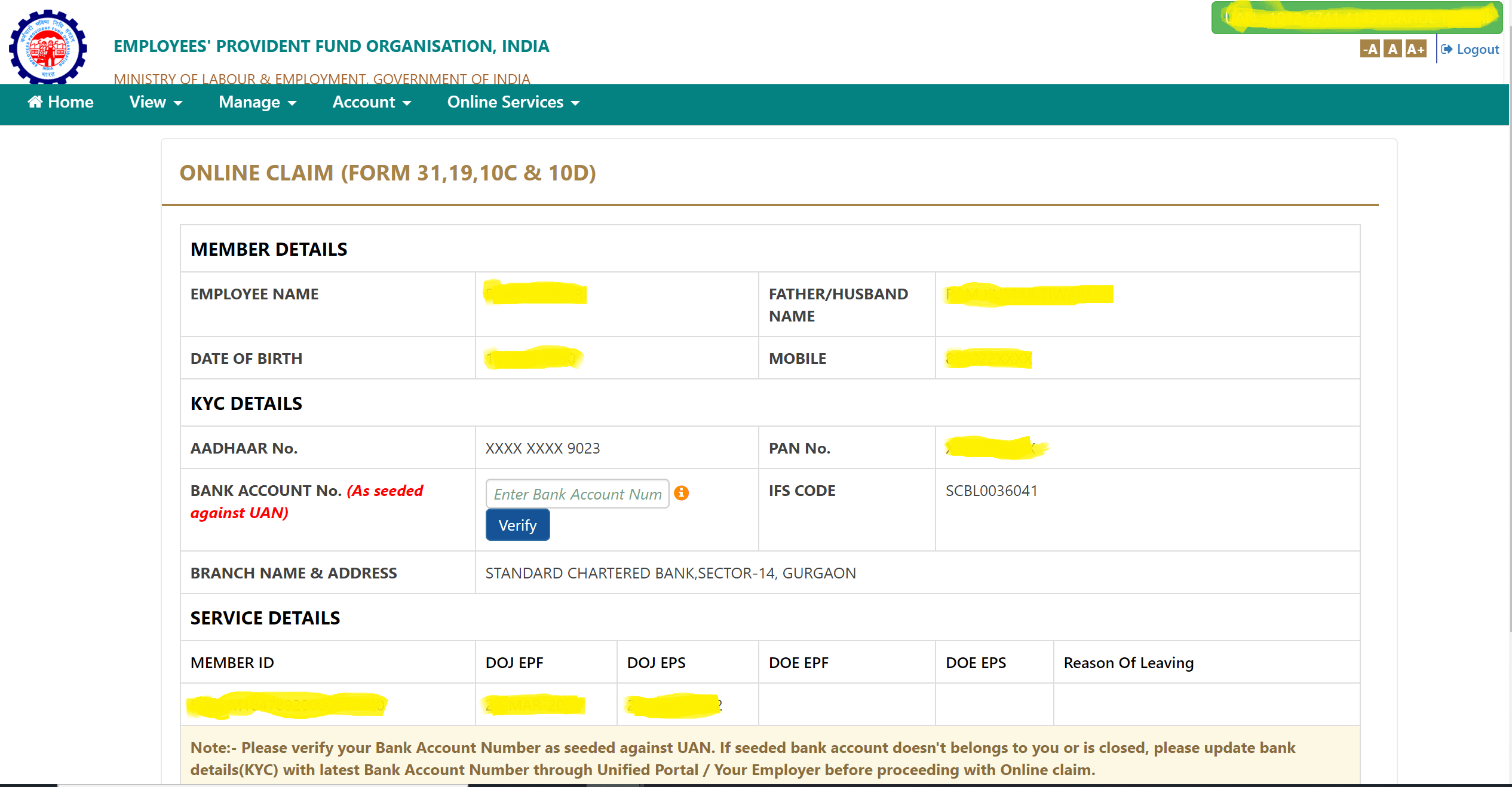

- Select From 19, 31 and 10C

Next, select ‘Claim Form – 19, 31 and 10C’. Enter your details such as Name, date of birth, mobile number, PAN card number, etc.

- Verify Bank Details

Check the details and verify the same after entering your bank details.

- Select the Reason for Advance EPF Claim

The next step involves choosing the type of claim. One must enter the amount and reason for premature withdrawal and submit a request for the same.

The EPFO officers will scrutinise the request and grant sanctions for the same. Upon sanctioning, the requested funds will be directly transferred to the beneficiary’s registered bank account. The time for the process is 15-20 days from the date of submitting a request.

It is important for employees to have their PAN and Aadhaar linked with the EPFO database to avail of the loan.

How to Apply for EPF Loan Offline?

Here are the steps to apply for an EPF loan offline:

- First, one needs to download the EPF loan form, i.e., Form- 31, from the EPFO portal.

- Next, individuals must fill in all the details like withdrawal amount, the reason for withdrawal, years in service, etc., and submit the form to their organisation or company.

- After going through the form, the organisation or company will forward the same to EPFO for further processing.

After EPFO approves the request, the amount is directly credited to the individual’s bank account.

Also Read

Documents Needed for EPF Loan

Individuals need the following documents to avail EPF loan:

- Form 10 – C: EPFO needs this form for pension withdrawal benefit.

- Form 19: It is required for the final provident fund settlement procedure.

- Form 31: This form is sufficient for any premature withdrawal from EPF. One does not need to present any more documents.

EPF Loan Eligibility

Eligibility criteria for EPF loans are given below:

| Reason for withdrawal | Withdrawal limit | Minimum years in service | Terms and conditions |

| Education | Up to 50% of an individual’s contribution in EPF. | 7 years | Individuals can utilise the amount for educational expenses of themselves or their children after class 10. |

| Marriage | Up to 50% of an individual’s contribution to the fund. | 7 years | One can use the funds for his/her own marriage or the marriage of a family member. |

| Purchase of land or house | House: Up to a maximum of 36 times of dearness allowance plus monthly salary.Land: Up to a maximum of 24 times of dearness allowance plus monthly salary. | 5 years | The property must be in the spouse’s name or the employee themselves or jointly owned by both. |

| Medical emergency | 6 times of dearness allowance plus monthly wages | N/A | Individuals can withdraw an amount to bear the medical expenses themselves or their family members. The patient must be in hospital for more than one month.In case of some serious illness, one can withdraw funds from EPF even without hospitalisation. |

| Home loan repayment | Up to 90% of employer and employee’s contributions in EPF | 10 years | The balance in the provident fund account, including interest, must be greater than Rs. 20,000. |

| Natural calamity | Up to a maximum of 50% of employee’s share in EPF. | N/A | The individual must have a certificate of damage. |

| Withdrawal before retirement | Up to an amount not more than 90% of the accumulated corpus, including interest | 57 years | One can utilise the amount for self-use only. |

What are the Conditions for EPF Loan/EPF Withdrawal?

One can withdraw from the EPF corpus for the following purposes, but there are certain rules:

1. Construction of House or Property

For land purchase, you can withdraw up to 24 times of basic monthly salary + dearness allowance. However, you can withdraw up to 36 times your monthly basic salary + dearness allowance for house purchases.

However, there are a few pointers to keep in mind:

- The land or house should be registered under the employee’s name or jointly with the spouse

- The construction should begin within 6 months and should be completed within 12 months of the last withdrawn instalment

- The amount can be withdrawn only once during the entire service duration

- Minimum 5 years of service required to be eligible

2. Education Purposes

You can withdraw up to 50% of your EPF contribution. However, there are a few factors you need to keep in mind:

- Purpose of withdrawal should be for either your or your child’s education (post matriculation)

- Minimum of 7 years of service is mandatory

3. Medical Treatment

You can withdraw six times your monthly basic salary or your total EPF contribution. There are no years of service conditions attached. The purpose of withdrawal should be solely for the medical treatment of self, spouse or children.

4. Marriage

You can withdraw up to 50% of your EPF contribution to meet marriage-related expenses. The conditions are as follows:

- Purpose should be to meet fund requirements for the marriage of self, brother/sister or son/daughter

- Minimum of 7 years of service is required

5. Home Loan Repayment

You can either withdraw 36 times your monthly basic salary + dearness allowance, or total EPF corpus along with interest or an amount equivalent to total outstanding principal and interest on your housing loan, whichever is lower. The conditions attached are as follows:

- The property should be registered under the employee’s name or spouse or jointly with spouse

- Withdrawal is only permitted upon furnishing your home loan documents as requested by the EPFO

- The total EPF amount along with interest accumulated in your account has to be above Rs.20,000

- More than 7 years of service is a prerequisite

Any serious loss one incurs due to a natural calamity is also a reason for which one can make a premature withdrawal from EPF.

6. Home Renovation

You can withdraw up to 12 times your monthly salary plus dearness allowance or your EPF contribution along with the interest or the total cost of home renovation, whichever is lower. The conditions attached are:

- The property should be registered under the employee’s name or spouse or jointly with the spouse

- You can avail of the facility twice – after 5 years of completion of the house and after 10 years of completion of the house

- Minimum 5 years of service is mandatory

7. Partial Withdrawal before Retirement

You can partially withdraw your EPF amount just before retirement as well. This can be done once you reach 54 years of age. The conditions attached are:

- Withdrawal of up to 90% of the accumulated corpus

- Withdrawal allowed just 1 year before retirement

Additionally, EPFO has the power to alter the rules and conditions for premature withdrawals. Recently, during the COVID-19 pandemic, EPFO allowed emergency withdrawals from EPF subject to terms and conditions.

Before we move on, in case you’re looking for emergency funds, instead of emptying your retirement savings accumulating in your EPF account, you can apply for a cash loan with Navi. You can get loans up to Rs.20 lakh in a 100% paperless manner with Navi. Download the Navi app today, apply and get the loan amount disbursed within minutes!

Also Read

EPF Loan Calculation

The calculation of an EPF loan is a simple process. Let’s consider an example which will help us understand the concept more clearly.

Suppose Mr Verma has an EPF balance of Rs. 2 lakh. Due to financial issues faced during the covid-19 pandemic, he wants to take an EPF loan.

His monthly salary is Rs. 20,000. Therefore, his salary for three months amounts to Rs. 60,000, and 75% of Mr Verma’s EPF balance is Rs. 1.5 lakhs.

The maximum limit of an EPF loan can either be 75% of the EPF balance or three months’ salary, whichever is less. In the case of Mr Verma, the lower amount is his three months’ salary; therefore, he is eligible for an EPF loan of up to Rs. 60,000.

How to Check EPF Loan Status Online?

Here are steps to check EPF loan status:

- One needs to visit the EPFO portal and go to the services section.

- In the services tab, an individual must choose the employees option.

- After that, users will be redirected to another page. They need to select the services tab again.

- Next, beneficiaries must visit the relevant section that allows them to check their loan status.

- After entering the credentials like UAN and PAN details, one can know the claim status.

COVID-19 Pandemic Emergency EPF Loan

The EPFO allowed a non-refundable advance for its members to deal with the financial stress during the COVID-19 pandemic. As economic activity receded, people were out of jobs and facing immense difficulty in meeting their basic expenses. So this emergency loan was allowed by EPFO to provide respite to individuals.

How to Claim Covid-19 EPF Emergency Advance?

Here are the steps that you need to follow to claim Covid-19 EPF Emergency Loan:

Step 1: Download Umang App from Google Playstore or iOS.

Step 2: Go to the section on EPFO from the menu.

Step 3: Select “Request for Advance (Covid -19)” from several options that are visible to you.

Step 4: The next step involves entering your UAN and clicking on the ‘Get OTP’ option.

Step 5: You can login to your account after submitting the OTP received on your registered mobile number.

Step 6: Once you are redirected, enter the last 4 digits of your EPF-linked bank account number. After that, you must select the appropriate member ID from the drop down list.

Step 7: Click on the “Proceed to Claim” option.

Step 8: Enter your permanent address, and click next.

Step 9: Thereafter, you must open Form-31. In that form, enter the required advance amount and upload an image of a cancelled cheque. All details on the cheque like, IFSC, account number, and bank branch name, should be clearly visible to the naked eye.

Step 10: Complete the declaration checkbox and submit the Aadhaar-based OTP received on your mobile phone.

Step 11: Select the submit option.

By following these steps, you can successfully file a claim for EPF emergency advance. However, as per government guidelines, you must complete E-KYC on the UAN member portal in order to avail this benefit.

Features of COVID-19 Premature Withdrawal

The features of this non-refundable advance were as follows:

Eligibility

Employees who are workers of a factory or an organisation affected by the COVID-19 outbreak in their area could claim this benefit. As the entire country was dealing with the pandemic, every employee was eligible to claim this relaxation.

Documents

Employees do not need to present or show any document to claim this benefit.

Quantum

Individuals can make a maximum withdrawal of up to 3 months’ sum of salary and dearness allowance or 75% of the accumulated balance in the fund, whichever is less.

EPF vs Personal Loan: Key Differences

Here are some differences between an EPF loan and a regular loan:

| Parameter | Loan against EPF | Personal loan |

| Definition | This is partial or full premature withdrawal from the accumulated EPF corpus of the employee. | It is a loan taken by a borrower at a specific interest rate which the borrower pays back within the loan tenure. |

| Interest | Individuals do not pay any interest as the withdrawal is from their corpus. | Borrowers have to pay interest depending on the type of loan availed. |

| Repayment | You are not required to repay the amount withdrawn from EPF. | A borrower is obligated to repay the loan amount within the stipulated loan tenure. |

Final Word

Premature withdrawals or loans against PF are an emergency measure to ward off an immediate financial crisis. It is a useful tool that allows one to use the accumulated savings to meet some specific financial requirements. To know about the above conditions as prescribed by EPFO, refer to the above sections.

In case you’re looking for an instant loan, apply for a Navi Cash Loan. You can get instant loans up to ₹20 lakh with Navi in a 100% paperless manner and with flexible repayment tenure.

FAQs

EPF contributions are mandatory for employees having a salary of up to Rs. 15,000. This is applicable only when the individual is working in an establishment having more than 20 workers. If individuals work in an organisation with less than 20 workers, enrolment in EPF is optional.

Employees having an EPF can avail of the benefit of EPF loans for up to a maximum of 3 times. However, in some cases like medical contingencies, natural calamities or lockouts, there is no limit on the number of times one can avail of this loan facility.

Employees can take advantage of the EPF loan facility even before the time period of 5 years. This is applicable when one has lost his/her job. Individuals can withdraw a maximum of 75% of the total amount after one month of being unemployed. This withdrawal or loan amount is taxable.

In case of a job change, the entire EPF balance is transferred to a new employer. The new employer will make monthly contributions to EPF. Individuals can also withdraw some amount from the EPF corpus if they provide a declaration that they won’t join a new job for the next six months.

Form 31 allows one to make a partial premature withdrawal from his/her EPF account. One needs to attach a doctor’s certificate for claiming a loan for medical reasons. In case of loan repayment, a declaration from the lender stating outstanding loans and interest must be attached with the form.

Personal Loan in Your City