General Provident Fund (GPF) 101: Guidelines, Interest Rate, How to Open an Account and Withdrawal Rules

If you are a Government employee, you can open a General Provident Fund (GFP) account. It is one of the three types of Provident Fund account – Public Provident Fund (PPF), General Provident Fund (GPF) and Employees Provident Fund (EPF). However, the terms and conditions, interest rates and rules of these three may vary.

So, how is GFP different from EPF and PPF? What is the interest rate of GPF? How to open a GPF account? And, what are the GPF withdrawal rules? Read on to find out!

What is General Provident Fund (GPF)?

General Provident Fund is a type of Public Provident Fund (PPF) account beneficial for every government employee. It enables government individuals to preserve a part of their salary in the General Provident Fund. The entire amount collected throughout the employment period is paid when the employee retires.

Characteristics of General Provident Fund

General Provident Fund facilitates government employees in many ways. Some of their essential features are:

- General Provident Fund can be given to any salaried individual.

- This scheme is controlled under the Ministry of Personnel, Public Pensions and Grievances by the Department of Pension and Pensioner’s Welfare.

- The individual is not required to submit any document while withdrawing the amount at the time of retirement.

- The department will offer a written document regarding immediate payment of the General Provident Fund money just after an individual’s retirement.

- A nominee is paid an extra amount at the time of death of the subscriber as per the guidelines of the General Provident Fund. However, this added amount should not be more than Rs. 60,000.

- After withdrawing, the money can be returned in small instalments each month towards the fund after withdrawing it.

- A subscriber has to mention the name of a nominee (family member) in the form while taking General Provident Fund.

- At present, the GPF interest rate of 7.10% is offered.

Guidelines and Rules of General Provident Fund

A person desiring to open a General Provident Fund account must go through these vital guidelines. They are:

- Subscribers are not allowed to contribute more than their income to the General Provident Fund account.

- A subscriber can mention more than one person as a nominee, but his/her GPF details must be cleared while signing the form.

- A person involved in services for at least a decade will be able to withdraw the preserved money before retirement.

- Anyone desirous to buy a new home or for loan repayment purposes can withdraw 75% of the GPF amount.

- The amount saved in the General Provident Fund account will mature at the time of the subscriber’s retirement.

Interest rates for General Provident Fund

The interest rate of the General Provident Fund varies from year to year. The following table shows rates of interest over the last 5 years:

| Financial Year | Interest Rate |

| 2017-2018 | 7.9% (April 2017-June 2017) 7.8% (July 2017-September 2017) 7.8% (September 2017-December 2017) 7.6% (January 2018-March 2018) |

| 2018-2019 | 7.6% (April 2018-September 2018) 6% (October 2018-March 2019) |

| 2019-2020 | 8% (April 2019-June 2019) 7.9% (July 2019-March 2020) |

| 2020-2021 | 7.10% |

| 2021-2022 | 7.10% |

Conditions for General Provident Fund

An individual who has met all of these following conditions is suitable for opening a General Provident Fund account:

- Must be an Indian resident beside a government employee.

- Government employees associated with a particular salary class are eligible for General Provident Fund.

- Employees associated with a private organisation are not eligible for General Provident Fund.

- The eligible employees must keep a certain part of their salary for becoming a GPF member.

How to Open a General Provident Fund Account?

Anyone can open a GPF account effortlessly. The Accountant General (AG) office is in charge of this account. Firstly, the person desiring to open an account has to fill up a specified form and submit it to the AG office. Later on, the office will provide them with their account number.

The office will further inform them about their monthly salary deductions to (Drawing and Disbursing Officer) DDO. Moreover, a statement of debits and credits, a GPF balance sheet, and accrued interest are sent to the employee at the end of the financial year.

How to Withdraw Money from a General Provident Fund?

The employees are free to apply to withdraw money from GPF online. This money will be credited to their respective bank accounts without any hassle. Furthermore, government employees can take away their money based on their years of service under the renewed provisions. This process will not require any further approval.

How to Check General Provident Fund Statement?

Here are some following steps you should follow while checking your GPF statement online:

- Visit EPFO Official Website

Visit the official website of EPFO and go to its homepage.

- Click on ‘Services’

On top menu bar, click on the tab ‘Services’. A dropdown menu will appear.

- Click on ‘For Employees’

From the dropdown menu, click on ‘For Employees’.

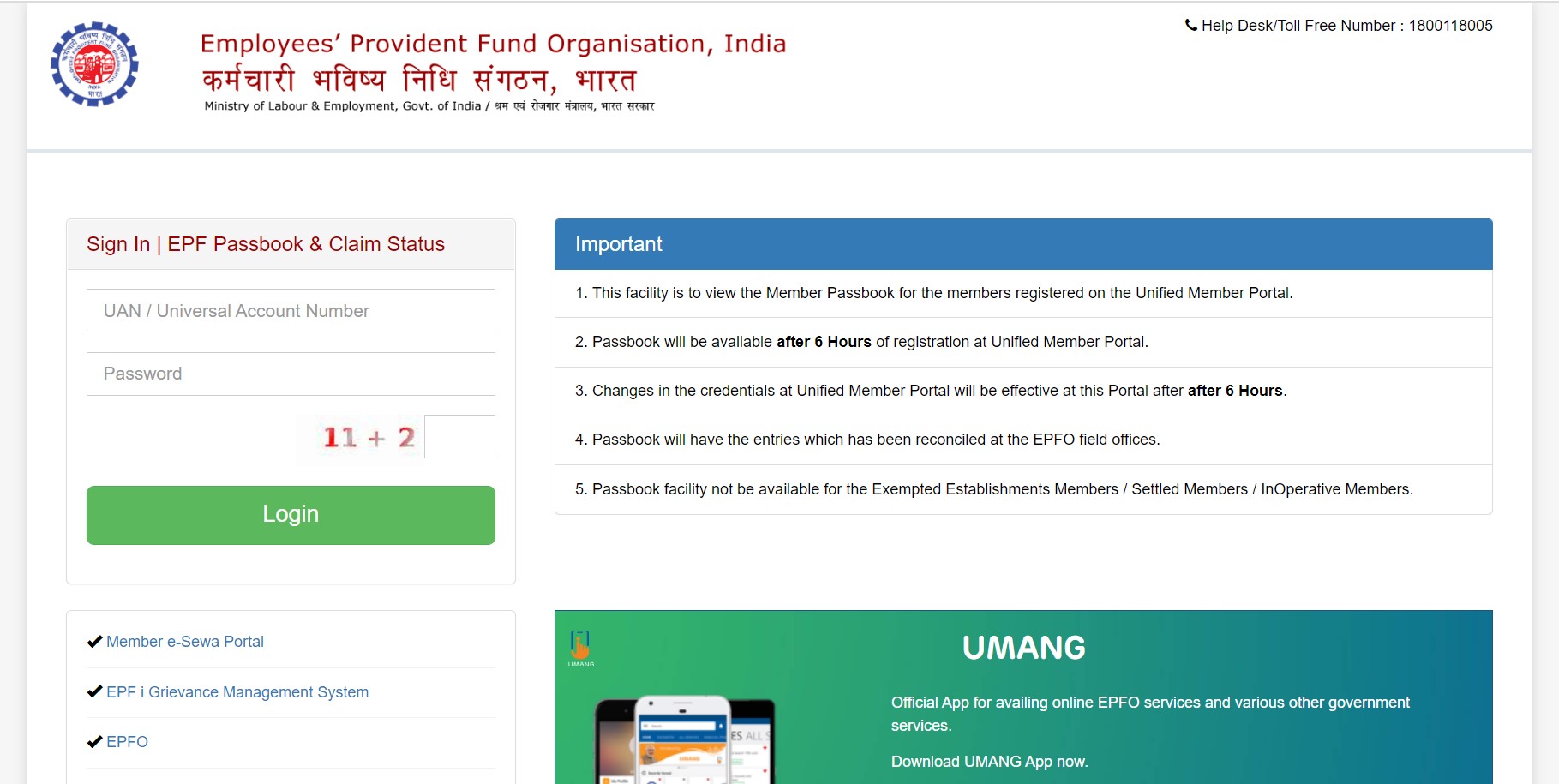

- Select ‘Member Passbook’

Scroll down. Under the ‘Services’ category, select ‘Member Passbook’. You will be directed to a new page.

- Enter Your Login Details

Enter your UAN and password.

Now, you can see your PF account’s details. You can either download the GPF status or simply view it.

Also Read: Tax Implications Of Provident Fund & How To Save Tax

Difference between General Provident Fund (GPF) and Employee Provident Fund (EPF)

The main differences between General Provident Fund and Employees’ Provident Fund are as follows:

| Aspects | GPF | EPF |

| Interest rate | 7.1% | 8.1% |

| Eligibility | Only government employees are eligible. | Only private sector employees are eligible. |

| Period of maturity | At the time of retirement | Up to the age of 58 years |

| Early cessation | On leaving the government job. | If unemployed for 2 months. |

| Limit of deposit | Minimum deposit amount should be 6% of the employee’s salary. | Minimum deposit amount should be 12% of the employee’s salary. |

Also Read: What Is A Voluntary Provident Fund And How Is It Different from EPF And PPF?

Final Word

GPF is a beneficial savings scheme organised by the Government for government employees. There is no telling when an individual will require money. So, it is better to stay in a safe zone. GPF helps employees accomplish their financial goals. It can be for family emergencies, marriage or even medical purposes.

FAQs on GPF

Ans: The full form of GPF is General Provident Fund.

Ans: Interest received during GPF is entirely tax-free and, no tax is imposed while withdrawing it.

Ans: General Provident Fund deducts 6% money from the basic salary of an individual.

Ans: An extra sum of money is added to the amount and credited to the account of his/her nominee.

Ans: No. Because the General Provident Fund scheme is only for the government employees.

Personal Loan in Your City