Loan-to-Value Ratio | Working, Calculation, Guidelines and Impact

The loan-to-value (LTV) ratio is a risk evaluation method used by financial institutions and lenders. It is the percentage of the property’s value that you will receive as a loan amount from your lender. Loan assessments with high LTV ratios are generally regarded as higher-risk loans. A higher LTV ratio increases the borrower’s risk, whereas a lower LTV ratio can help one get better loan terms, including lower interest rates on their home loan.

Read on to understand how LTV ratio works, how to calculate it,

How Does Loan to Value Ratio Work?

The higher the loan amount, the greater the LTV ratio. This in turn leads to a greater risk on the lender’s part. If you are deemed a higher risk by the lender, it usually implies:

- It is more difficult to obtain loan approval.

- You may be required to pay a higher rate of interest.

- You may be required to pay additional fees, like mortgage insurance.

LTV is usually calculated while dealing with a loan backed by some kind of collateral. When you borrow to purchase a house, the loan is secured by a mortgage on the house. If you are unable to make payments, the lender may seize and sell your property through foreclosure. The same is true for car loans, wherein upon failing to make payments, the car may be seized. This is because lenders want to rest assured that in the event of a default, they can retrieve their money back in some way.

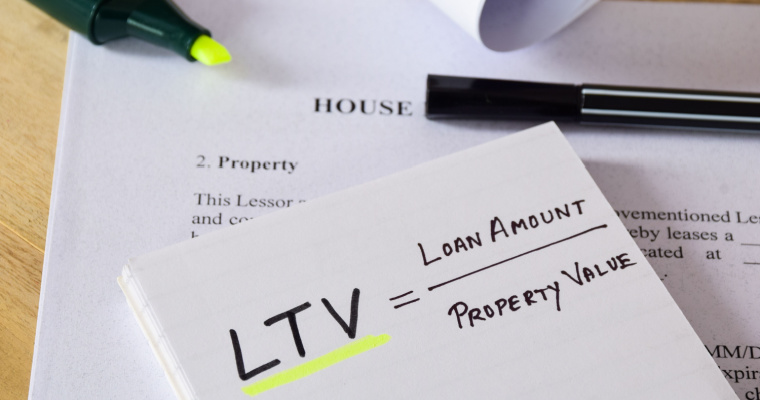

How to Calculate the Loan to value ratio?

The Loan to value ratio formula is given as follows:

(Loan Amount / Asset Value) * 100 = LTV%

For example, if a borrower urgently seeks a loan against property of Rs.1 crore, and the lender determines the amount to be sanctioned to be Rs.80 lakh, the LTV ratio would be equal to:

(1,00,00,000/80,00,000) x 100 = 80% LTV

What is a Good LTV?

Most lenders consider 80% to be an acceptable loan-to-value (LTV) ratio. Anything less than this figure is preferable. Borrowing costs may increase or borrowers may be rejected loans if the LTV exceeds 80%.

In general, lenders prefer to sanction home loans with lower LTV percentages since they lessen default risk for lenders. As a result, choosing a lower LTV ratio can boost one’s home loan eligibility. Some lenders also offer reduced rates of interest to applicants who choose lower LTV ratios. Furthermore, lower LTV ratios equate to smaller loan amounts, which, when combined with lower interest rates, can dramatically reduce your entire interest expense.

How Does Loan-to-Value Ratio Affect Interest Rates?

Lenders in the U.S. use a strategy known as “risk-based pricing,” wherein charging a higher interest rate on loans is seen as fairly risky. Borrowers with poor credit are charged higher than those who have excellent credit, and this also applies to LTV: Because a high loan-to-value implies a greater risk to the lender, loans with high LTVs often have higher rates of interest.

How Does Loan-to-Value Ratio Impact Eligibility

One’s home loan eligibility is intricately linked to their LTV ratio. The lenders evaluate the requested amount based on the borrower’s LTV eligibility. Here are some things to consider when applying for a home loan:

- Make a sizable down payment to borrow a smaller principal amount and lower your overall cost of borrowing.

- Evaluate your loan amount application and make sure the LTV ratio does not exceed the lender’s disbursal policy. It should be noted that applicants with a high LTV may have a larger possibility of rejection, as a high LTV represents greater risk for the lender.

- In order to increase your Home Loan eligibility, seek for a joint Home Loan with co-applicants. If your income or repayment capability is insufficient, or the property value is very high, a joint application may be the best option, as the lender can depend on all co-applicants for better eligibility.

RBI Guidelines on LTV

The RBI’s guidelines state that the LTV ratio for home loans can be up to 90% of the value of the property for loan amounts of Rs.30 lakh and lower. Additionally, the LTV ratio ceiling has been established at 80% for loan amounts greater than Rs.30 lakh and up to Rs.75 lakh, and 75% for loan amounts greater than Rs.75 lakh.

This means that if the LTV ratio is 90%, you will have to pay at least 10% of the property value out of your own pocket, with the remainder being covered by a house loan. The LTV ratio is therefore used to calculate the minimum down payment required when acquiring a home or property.

Final Word

In addition to one’s credit, their debt-to-income ratio (obtained by dividing the debt payments by income) is another way of determining the affordability of a new loan. Calculating the LTV ratio is an important part of mortgage underwriting. It can be used when purchasing a new home or refinancing an existing mortgage into a new loan.

Lenders use the LTV ratio to ascertain the risk level they are willing to assume when underwriting a mortgage. When borrowers seek a loan for a sum that is at or near the assessed value (and thus has a higher LTV ratio), lenders believe that the loan is more likely to default. This is due to the fact that the property contains very little equity. As a result, in the case of a foreclosure, the lender may struggle to sell the property for enough to clear the outstanding mortgage sum while still making a profit.

FAQs

Ans: LTV meaning is a ratio that is used as a risk evaluation method by financial institutions as well as other lenders prior to authorising a mortgage. It is the percentage of the property’s value that you will receive as a loan amount from your lender.

Ans: The LTV ratio formula is given as follows:

(Loan Amount / Asset Value) * 100 = LTV%

Ans: Most lenders consider 8% to be an acceptable loan-to-value (LTV) ratio. Anything less than this figure is preferable. Borrowing costs may increase or borrowers may be rejected loans if the LTV exceeds 80%. In general, lenders prefer to sanction home loans with lower LTV percentages since they lessen default risk for lenders.

Ans: Borrowers with poor credit are charged higher than those who have excellent credit, and this also applies to LTV: Because a high loan-to-value implies a greater risk to the lender, loans with high LTVs often have higher rates of interest.